The $300 Billion Pivot: How APAC Telcos Are Reinventing Themselves in the Enterprise Era

Asia-Pacific telecom operators are making a $300 billion pivot from traditional consumer services to enterprise-focused solutions. With growing demand for cloud, 5G, and digital infrastructure, telcos across the region are redefining their value proposition to serve enterprises with high-margin.

What happens when connectivity plateaus, but enterprise tech demand explodes? Telcos across APAC are rewriting their playbooks, and those who move first will define the next growth era.

15 Slides | Sector Benchmarks | Opportunity Sizing | Strategic Blueprints

WHO THIS POV IS FOR

This report is for decision-makers responsible for redefining telecom business models, capturing B2B market share, and leading digital platform transitions across Asia-Pacific.

Ideal for:

- CXOs & Strategy Officers at telecom, cloud, and ICT firms

- Heads of Digital Transformation & Enterprise Services

- Platform Leaders in IoT, Edge, Cloud, and Cybersecurity

- Investors & M&A Professionals seeking the next telco-to-techco breakout stories

EXECUTIVE SUMMARY

The B2C chapter of telecom is nearing its end in APAC. With subscriber growth flattening at under 4% and voice/data ARPU falling across major economies, telcos can no longer rely on legacy connectivity models.

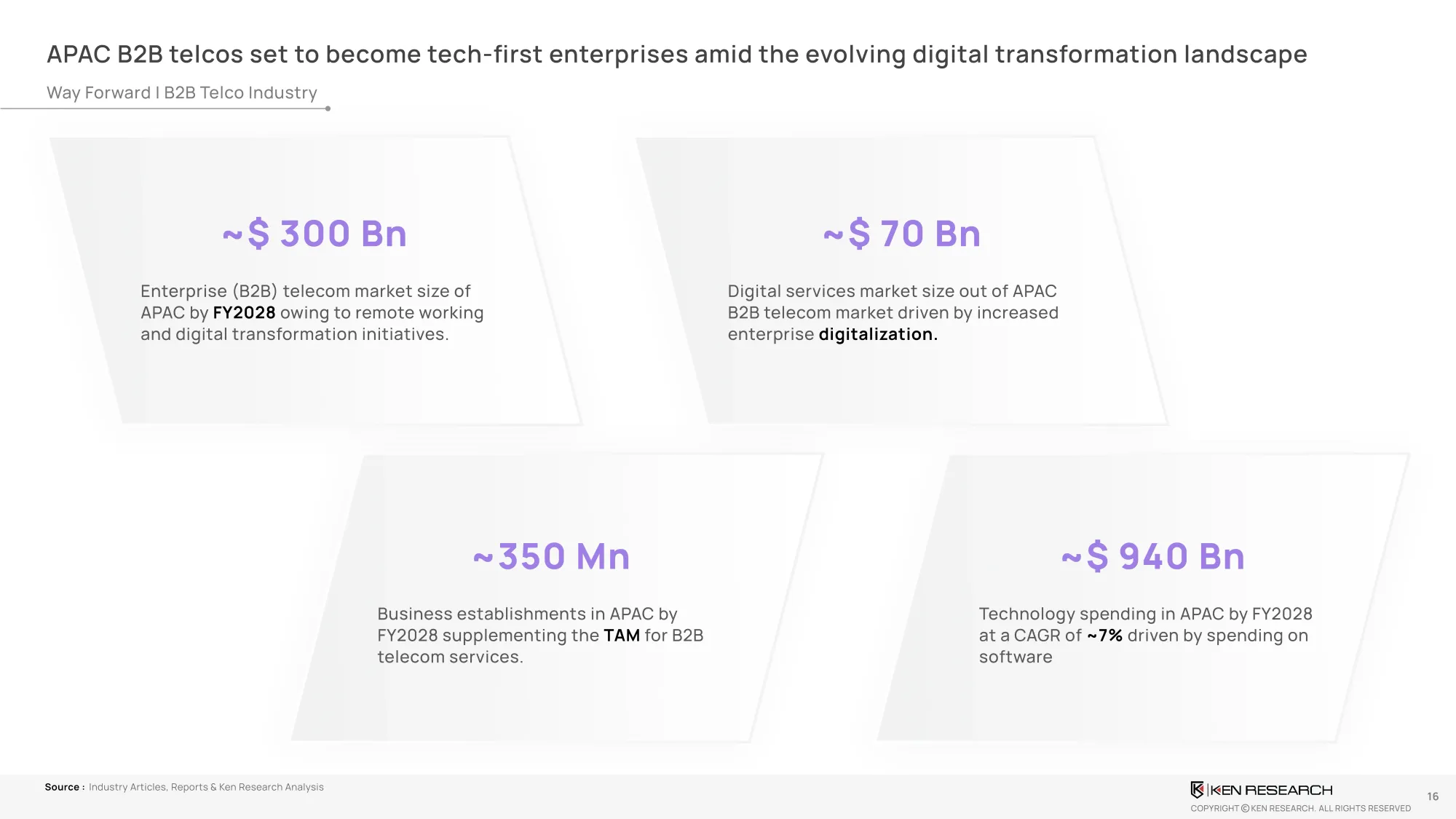

What’s rising in its place is a $300 billion enterprise market, with a core $70 billion digital services sub-segment fueled by demand for cloud, IoT, and security. APAC is uniquely positioned: 67% of enterprises in the region expect to increase their telecom-tech spending, surpassing global intent (62%).

The opportunity is not just large—it’s urgent. Telcos that realign now toward enterprise-first growth will benefit from 6–8x higher ARPU, stickier multi-year contracts, and relevance in a tech-first enterprise world.

MARKET SNAPSHOT: ENTERPRISE IS THE NEW CORE

With B2C revenues stalling, the APAC telecom enterprise market is projected to reach USD 300 billion by FY2028. At the center of this evolution is digital enablement:

- Cloud, Cybersecurity, IoT, and Managed Services are driving a USD 70 billion opportunity, with CAGR rates between 12%.

- Meanwhile, legacy mobile internet and broadband have dipped below 4% annual growth, with many markets reaching >90% penetration.

What’s the shift? Telcos are transforming from bandwidth providers into trusted IT service orchestrators. This POV explores how you can lead—not follow—that transition.

THE DIGITAL SERVICES BREAKOUT: WHERE THE MONEY IS MOVING

APAC enterprise clients are now bundling network + cloud + security in a single SLA, triggering a reshuffle in revenue streams:

- Cloud & Managed Services now contribute one-third of enterprise revenue for APAC leaders like Singtel and NTT.

- Cybersecurity is expanding at 20–25% YoY, with BFSI and government leading the charge.

- IoT market in APAC are poised to hit USD 545 B by 2027, driven by manufacturing and smart cities.

If your product portfolio hasn’t shifted accordingly, your margins will.

PRODUCT STRATEGY: FROM PIPE TO PLATFORM

Top-performing telcos in the region are shifting from static bandwidth sales to modular enterprise services:

- Instead of “speed + data” plans, they offer Private 5G, Edge Compute, SASE, Managed SOCs, and Multi-cloud Orchestration.

- These services drive multi-year B2B contracts, increase cross-sell rates by 2.8x, and improve EBITDA margins by 5–8%.

Success is no longer about coverage—it’s about capability packaging.

WHO’S WINNING: APAC TELCO CASE STUDIES

Real examples show the transformation is already underway:

- Singtel: 50%+ of enterprise segment revenue now from digital services; leading in 5G MEC rollouts and hyperscaler marketplaces.

- NTT: Operating as a full digital integrator, offering cybersecurity + cloud + IoT across ASEAN.

- PLDT: Doubled cybersecurity services revenue in 2 years with new secure access and CPaaS bundles.

These players didn’t wait—they invested, restructured, and won new share.